“Sir, We Crossed the GST Limit… What Should We Do Now?”

- Abhinav Pradeep

- 9 minutes ago

- 4 min read

In my daily work, one thing I notice very often is this:

Most business owners do not ignore GST intentionally.They are usually busy running the business, handling customers, managing staff, checking payments, following up with suppliers, and somehow, GST limits get missed.

But GST does not wait.

Once a limit is crossed, the responsibility starts. If we notice it late, then the problem begins notices, penalties, blocked ITC, wrong invoicing, or pending compliance.

Let me explain this through some common situations that business owners usually come with.

1. “Sir, our sales crossed ₹40 lakh. Do we need GST registration?”

This is one of the most common questions.

A small trader may start with limited sales. Slowly, business improves. More orders come in. By the time they check properly, turnover has already crossed ₹40 lakh.

For goods, the GST registration limit is generally ₹40 lakh.For services, it is generally ₹20 lakh.

So, if you are doing business, you should not check GST registration only at year-end. You should monitor turnover every month.

Because once the limit is crossed, GST registration may become mandatory.

2. “We are a service business. Our income is only ₹22 lakh. Is GST applicable?”

Many service providers think GST applies only after ₹40 lakh.

That is not correct.

For services, the normal GST registration limit is ₹20 lakh. So even if the business looks small, GST may become applicable once service income crosses the limit.

This mainly affects consultants, freelancers, agencies, professionals, repair service providers, and other service businesses.

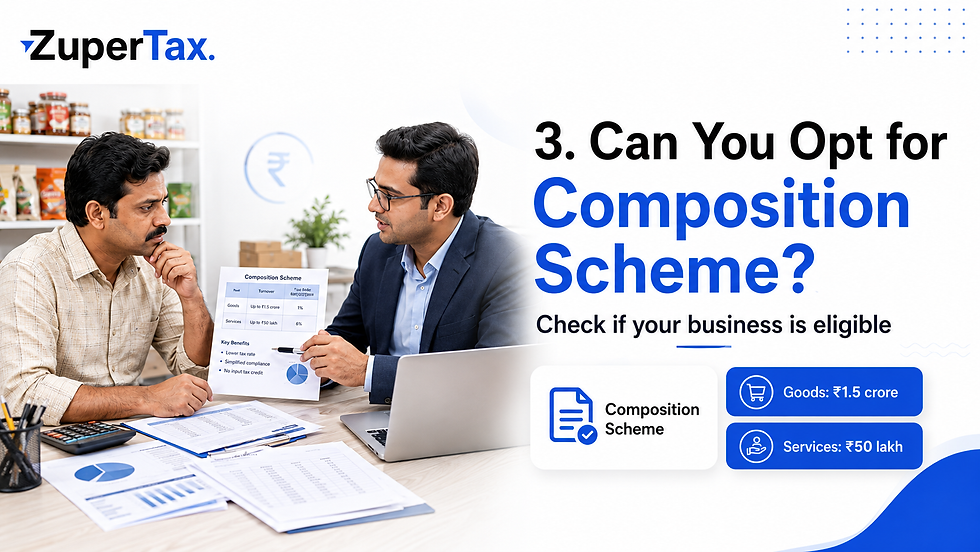

3. “Sir, can we go for composition scheme?”

Some small businesses come and ask whether they can pay GST under composition scheme because it is simpler.

Yes, composition scheme is available, but only if the business is eligible.

For traders and manufacturers, the composition scheme limit is generally ₹1.5 crore.For certain service providers, the limit is ₹50 lakh.

But composition scheme is not suitable for everyone.

If your customers are mostly businesses who need GST input, normal GST may be better. Under composition scheme, you cannot collect GST separately and your customer cannot claim ITC.

So before selecting composition scheme, we should check the customer type, margin, turnover and business model.

4. “Our turnover crossed ₹5 crore. Do we need e-invoice?”

Many businesses miss this point.

They continue preparing normal tax invoices even after crossing the e-invoice limit.

At present, e-invoicing is applicable when aggregate turnover crosses ₹5 crore in any financial year from 2017–18 onwards.

This is very important for B2B invoices.

If e-invoice is applicable and invoice is issued without IRN, the invoice may not be considered valid for GST purposes. This can also create issues for the customer’s ITC.

So, if your turnover is nearing ₹5 crore, do not wait. Start preparing your accounting and billing system in advance.

5. “Goods are moving for ₹70,000. Is e-way bill required?”

Another common issue comes during transportation of goods.

Generally, if the consignment value exceeds ₹50,000, e-way bill is required.

Many businesses remember GST invoice but forget e-way bill. This can create problems during vehicle checking and goods movement.

So, before dispatching goods, always check:

Is the goods value above ₹50,000?Is e-way bill required?Are invoice details and vehicle details correct?

A small mistake here can create unnecessary penalty and delay.

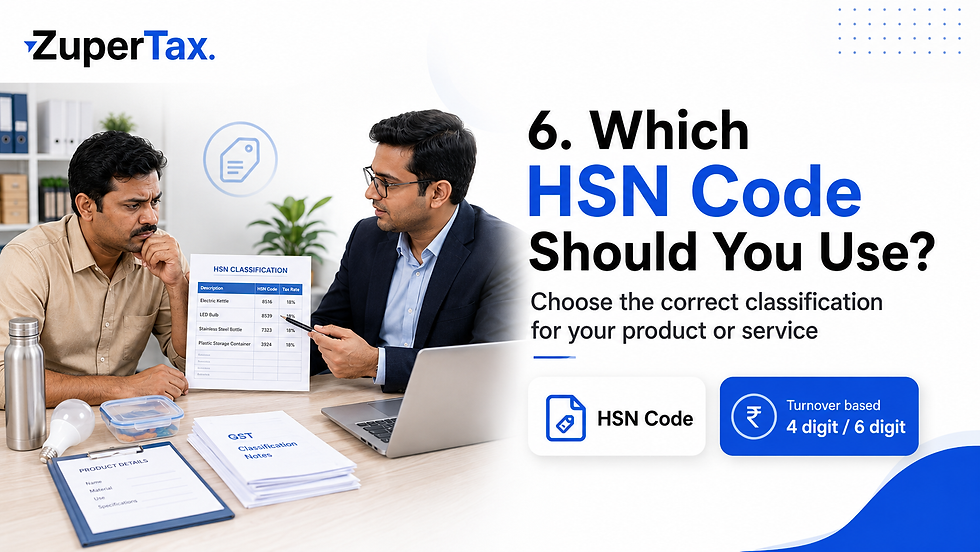

6. “Sir, which HSN code should we use?”

HSN is also a regular confusion.

Some businesses use 2-digit code, some use 4-digit code, and some do not use proper HSN at all.

The HSN requirement mainly depends on turnover.

If turnover is up to ₹5 crore, 4-digit HSN is generally required for B2B supplies.If turnover is more than ₹5 crore, 6-digit HSN is required.

Wrong HSN can create issues in GST return filing, e-invoice, notices and classification of GST rate.

So, HSN should not be selected casually. It should match the actual product or service.

7. “We forgot to claim ITC. Can we take it now?”

This is one of the most painful situations.

A client may come later and say:

“Sir, purchase bill is there, GST is paid, but ITC was not claimed.”

The problem is that ITC has a time limit.

Generally, ITC for a financial year should be claimed on or before 30th November of the next financial year, or before filing annual return, whichever is earlier.

So, ITC should be reviewed every month.

Do not wait until annual return. By that time, some credits may become time-barred.

8. “Sir, do we need to file GSTR-9 and GSTR-9C?”

Many taxpayers file monthly or quarterly GST returns, but forget annual compliance.

Normally:

GSTR-9 applies when turnover exceeds ₹2 crore.GSTR-9C applies when turnover exceeds ₹5 crore.

This is where proper reconciliation becomes important.

Sales as per books, GSTR-1, GSTR-3B, e-invoice, e-way bill and financial statements should match properly. Otherwise, difference may come later during notice or scrutiny.

9. “Our GST registration got cancelled. Can we restore it?”

Sometimes businesses miss return filing continuously and GST registration gets cancelled by the department.

After that, they come and ask whether it can be restored.

Yes, revocation can be applied within the permitted time limit. Normally, application should be filed within 30 days, with possible extension in eligible cases.

But the better approach is simple:

Do not let GST returns remain pending for long.

Once registration is cancelled, the business may face invoice issues, customer issues, e-way bill issues and compliance burden.

10. “Sir, can we pay full GST using ITC?”

Not always.

Rule 86B says that in certain high-turnover cases, if taxable supplies exceed ₹50 lakh in a month, the taxpayer may be required to pay at least 1% of output tax liability in cash, subject to exceptions.

Many businesses think that if ITC is available, no cash payment is required.

But this rule has to be checked carefully for applicable cases.

Final Thought

GST compliance is not only about filing returns.

It is about watching the limits at the right time.

A business owner should regularly check:

GST registration limit

Composition scheme eligibility

E-invoice applicability

E-way bill requirement

HSN code requirement

ITC claim deadline

Annual return applicability

Refund time limit

Revocation time limit

Rule 86B cash payment requirement

Most GST problems do not happen in one day.

They happen because small limits are missed month after month.

So, if you are running a business, do not wait for a notice to check GST compliance.

Review your GST position regularly, take timely action, and stay compliant.

Need help reviewing your GST compliance?

You can contact ZuperTax for GST registration, return filing, reconciliation and compliance support.

Comments